Hereditary Cancer Testing Industry: Advancing Preventive Oncology through Genetic Insights

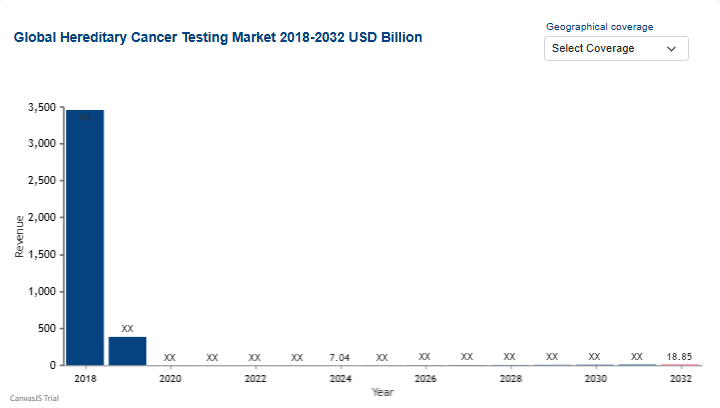

The growing emphasis on personalized medicine and proactive risk management is driving a significant expansion in genomic screening. The Hereditary Cancer Testing Market was valued at USD 7.04 billion in 2024 and is projected to reach USD 18.85 billion by 2032, growing at a CAGR of 20.87% during the forecast period of 2025 to 2032. This growth is fueled by the falling costs of genomic sequencing and an increased clinical awareness of how inherited genetic mutations significantly elevate lifetime cancer risks.

Hereditary cancer testing identifies specific germline mutations—such as BRCA1, BRCA2, or those associated with Lynch Syndrome—that are passed down through families. By identifying high-risk individuals before cancer develops, healthcare providers can implement intensive surveillance, chemoprevention, or risk-reducing surgeries, fundamentally shifting the oncology paradigm from reactive treatment to proactive prevention.

Request a sample of the "Hereditary Cancer Testing" report @ https://www.databridgemarketresearch.com/nucleus/request-a-sample/global-hereditary-cancer-testing-market

Key Market Drivers

The expansion of the genetic testing sector is characterized by the rise of comprehensive panels and institutional adoption:

Dominance of Multi-Panel Tests: Multi-Panel Test is both the largest and fastest-growing test segment (USD 4.60 billion in 2024; 21.27% CAGR). Clinicians are increasingly moving away from single-site tests in favor of panels that screen dozens of genes simultaneously to provide a more holistic risk profile.

PCR Technology Leadership: Polymerase Chain Reaction (PCR) remains the leading and fastest-growing technology segment (USD 4.52 billion; 21.35% CAGR), valued for its reliability, speed, and cost-effectiveness in amplifying genetic material for analysis.

Hospital-Centric Care: Hospitals represent the largest and fastest-growing end-user segment (USD 2.58 billion; 21.78% CAGR). As genetic counseling becomes a standard part of oncology departments, hospitals are centralizing testing workflows to improve patient outcomes.

Direct Tender Efficiency: Direct Tender is the dominant distribution channel (USD 4.78 billion; 21.04% CAGR), reflecting large-scale procurement by government health programs and private hospital networks to standardize genetic screening protocols.

Breast and Ovarian Focus: Hereditary Breast & Ovarian Cancer Syndrome is the largest and fastest-growing disease segment (USD 3.99 billion; 21.52% CAGR), driven by high public awareness and established clinical guidelines for BRCA testing.

Market Segmentation and Scope

The industry is strategically organized to address a spectrum of hereditary syndromes through advanced diagnostic technologies:

By Disease: Includes Hereditary Breast & Ovarian Cancer Syndrome (leading), Lynch Syndrome, Cowden Syndrome, Li-Fraumeni Syndrome, and others.

By Test: Categorized into Multi Panel Test (leading) and Single Site Genetic Test.

By Technology: Spans Polymerase Chain Reaction (PCR) (leading), Sequencing, and Microarray.

By Diagnosis: Divided into Biopsy (leading), Lab Tests, and Imaging.

By Distribution Channel: Includes Direct Tender (leading) and Retail Sales.

By End Users: Primarily driven by Hospitals (leading), followed by Diagnostics Centers, Clinics, and Laboratories.

Implies a trial or illustrative record-specific data @ https://www.databridgemarketresearch.com/nucleus/request-a-sample/global-hereditary-cancer-testing-market

Competitive Landscape and Emerging Opportunities

The competitive environment is shifting toward Next-Generation Sequencing (NGS) and AI-Driven Interpretation. Leading diagnostic firms are utilizing NGS to decode entire exomes, while AI algorithms help variants of uncertain significance (VUS) to be classified more accurately. There is a significant opportunity in Lynch Syndrome and Hereditary Leukemia testing, where early identification can lead to life-saving colonoscopies or specialized hematologic monitoring.

Emerging opportunities are particularly strong in the Biopsy diagnosis segment (growing at 21.23%). As liquid biopsy technology matures, the ability to detect germline mutations alongside somatic mutations from a simple blood draw is streamlining the diagnostic journey. Additionally, the rapid growth in Multi-Panel Tests (growing at 21.27%) highlights an opportunity for manufacturers to develop "pan-cancer" panels that assess risks across multiple organ systems in a single clinical assay.

Regional Analysis

United States: Holds a leading position in revenue, valued at USD 2,413.39 million in 2024. The U.S. market is driven by high levels of genetic literacy, a robust insurance reimbursement landscape, and the presence of pioneering molecular diagnostic laboratories.

Europe: Focuses heavily on integrating hereditary testing into national cancer screening programs, with a strong emphasis on ethical data management and equitable access to genetic counseling.

Asia-Pacific: Anticipated to be a major growth engine as countries like China and India invest in large-scale genomic initiatives and increase healthcare spending on specialized oncology centers.

Frequently Asked Questions (FAQs)

1. Why are "Hospitals" the fastest-growing end-user segment? With a growth rate of 21.78%, hospitals lead because they are increasingly integrating genetic services directly into the oncology care continuum. By providing testing on-site, hospitals can ensure that genetic results immediately inform surgical decisions (e.g., prophylactic mastectomy) and personalized treatment plans.

2. What is driving the shift toward "Multi-Panel Tests"? Multi-panel tests (valued at USD 4.60 billion) are leading because many hereditary cancers are polygenic. Screening for a single gene often provides an incomplete picture. Multi-gene panels offer better "diagnostic yield," catching mutations that single-site tests would miss, often at a comparable price point.

3. Why does "Polymerase Chain Reaction (PCR)" remain the dominant technology? PCR (valued at USD 4.52 billion) is the leader due to its ubiquity in clinical labs. While sequencing is essential for discovery, PCR is the workhorse for validating known mutations and performing targeted site testing. Its maturity, high sensitivity, and lower infrastructure requirements make it the standard for high-volume clinical diagnostics.

Regional report :

Asia-Pacific Hereditary Cancer Testing Market

Europe Hereditary Cancer Testing Market

North America Hereditary Cancer Testing Market

Middle East & Africa Hereditary Cancer Testing Market

South America Hereditary Cancer Testing Market

Argentina Hereditary Cancer Testing Market

Australia Hereditary Cancer Testing Market

Belgium Hereditary Cancer Testing Market

Brazil Hereditary Cancer Testing Market

Canada Hereditary Cancer Testing Market

China Hereditary Cancer Testing Market

About Us: Data Bridge is one of the leading market research and consulting agencies that dominates the market research industry. Our company’s aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups across the world.

Contact: Data Bridge Market Research Private Ltd. 3665 Kingsway — Suite 300 Vancouver BC V5R 5W2 Canada +1 614 591 3140 (US) +44 845 154 9652 (UK) Email: Sales@databridgemarketresearch.com

Website: https://www.databridgemarketresearch.com/